Probably the biggest benefit that comes from having an annuity is the fact that it can pay you an income for the rest of your life. Even if you live so long that you completely exhaust the funds in the plan, the insurance company will continue paying you each year.

But what happens if you are unlikely to live for 20 or 30 years? What if you only expect to live for 10 years, or maybe even five? This can be a possibility if you have a health condition that is likely to shorten your life.

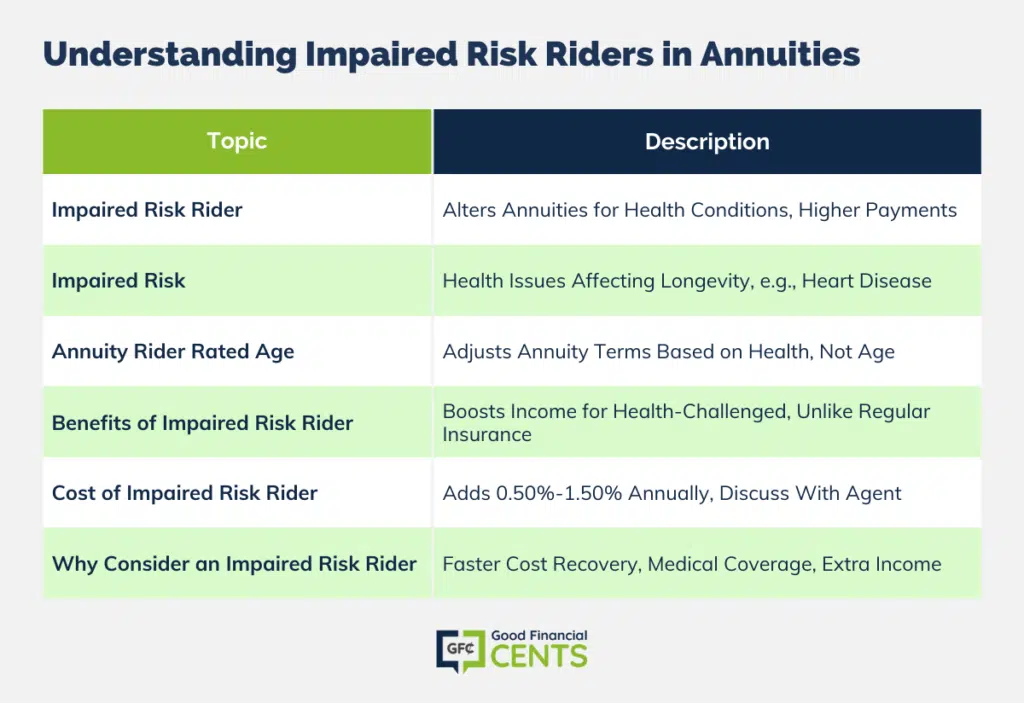

And for that reason, the insurance industry offers the impaired risk rider to go along with your annuity.

Table of Contents

What Is an Impaired Risk Rider, and How Does It Work?

Annuities are typically set up to provide an income in retirement. At age 65, the most common retirement age, the average person can expect to live for another 20 to 30 years. That means that they will need an income that will last that long and that won’t run dry at any time.

But not everyone can expect to live for several decades once they retire. If you have some sort of impaired health condition, it can shorten your lifespan. So what happens if, instead of living for another 20 years or more, you’re only expected to live for another 10 years?

As is normally the case with annuities, the unused funds in the plan will resort to the insurance company. This is actually a trade-off to counterbalance the possibility that you will outlive the value of your annuity. And if you don’t expect to live for at least 20 years, an annuity can be a losing proposition.

But that’s what the purpose of the impaired risk rider specifically addresses.

That means that you will actually receive higher payments than a person of the same age who has no health impairing conditions. Alternatively, the rider may entitle you to the same income payments that a healthy person would receive, but you would pay less for the annuity.

The rider results in a shorter income payout term for the annuity, which enables either the higher payments or the lower premium.

If you decide to add the impaired risk rider, your annuity will be medically underwritten (this is usually not required on most types of annuities).

The insurance company will do a medical evaluation to determine the impact of your particular health condition(s) on your expected longevity. They will use this evaluation to determine your rated age (see next section for how this works).

The rated age will be something less than normal longevity for your age. The insurance company will then base the income payout period on that age.

Since it will be shorter than would be the case for a completely healthy person, the insurance company will be in a position to either lower the premium or increase the annual income payment.

An impaired risk rider is typically added to an immediate annuity, which, as the name implies, is an annuity that begins making income payments as soon as the annuity premium has been paid.

What Is Impaired Risk?

An impaired risk is any health condition or related factor that is likely to reduce your longevity. Since there is an abundance of data available, the effect of common health conditions can be estimated with a high degree of accuracy.

This can include health impairments such as heart disease, cancer, stroke, alcoholism, leukemia, cirrhosis of the liver, high blood pressure, and many other health conditions.

But apart from health conditions that you may have, the insurance company will also evaluate other risk factors in determining the degree of impaired risk. Those conditions can include:

- Certain lifestyle behaviors, such as tobacco use, alcohol consumption, and drug use

- Genetic factors, including a family history of major diseases

- A history of reckless driving, including an excessive number of accidents, citations, and moving violations

- Participation in dangerous hobbies, such as skydiving, deep-sea fishing, mountain climbing, and any other activity that carries an increased risk of premature death

- Dangerous occupations, such as police and firemen, construction work, and roofing

- A history of traveling to foreign countries deemed to be dangerous

Annuity Rider Rated Age

Your chronological age is your actual age based on your birth certificate. But your rated age is something like your biological age – that is, it’s your age based on your actual physical condition.

It actually varies in most people since even small impairments or advantages can either increase or decrease your life expectancy.

But if you have a recognized and chronic health condition, the insurance industry is able to assess, based on actuarial records, your rated age. So, for example, if you are 65 years old and you have a serious heart condition, the insurance company might assign you a rated age of 75.

If you will be expected to live to be 85 if you are completely healthy, the company would determine – based on your health condition – that you are likely to live for only another 10 years.

The Benefits of an Impaired Risk Rider

As I wrote earlier, the primary benefit of an impaired risk rider is that it can result in either a higher income payment than a healthy person would receive or a lower premium paid in order to purchase the same income payment as a healthy person.

Recognizing that a person with impaired health will not live as long as a healthy person and will, therefore, be getting income payments for less time, the insurance company is able to accelerate those payments, resulting in a higher annual income.

This works in the exact opposite direction of traditional life insurance. For example, if you are a smoker and you are looking to buy a life insurance policy, you will be charged more for the premium. The alternative would be to purchase a much smaller life insurance policy for the same annual premium.

But if you have an annuity with an impaired risk rider, being a smoker will work to your advantage. Since it statistically indicates a shorter lifespan, the insurance company will be able to provide you with higher annual income payments.

The biggest benefit of an impaired risk rider is one that can’t be known at the time you take your annuity.

That’s the possibility that you will live longer than the insurance company expects and will, therefore, collect more in income payments than you paid for the premium to buy the annuity in the first place.

This is actually not an infrequent situation. Many people live longer than their life expectancy despite having impaired health.

Part of the reason is improvements in medical treatments. A new medication or surgical method can add years to the life of a person, even if they have a serious health problem.

It is entirely possible that you can even live a full life despite your health condition. And if you do, you stand to gain much more from your annuity than what you paid into it.

The insurance companies are actually well aware of this situation. This is the reason why relatively few insurance companies offer an impaired risk rider.

Given that lifespans, in general, have been increasing and that medical technology and treatments have been steadily improving, it is entirely possible that someone with a serious health condition can live much longer than expected.

The Cost of an Impaired Risk Rider

Adding an impaired risk rider to your annuity can cost between 0.50% and 1.50% of your annuity value on an annual basis.

So if the cost of your rider is expected to be 1.00%, and your annuity will provide an annual return of 6.00%, you will actually receive a return of 5.00%, net of the cost of the impaired risk rider.

Why You Might Want to Add an Impaired Risk Rider to Your Annuity

If you have an annuity or you plan to buy one, and you have a major health impairment, then an impaired risk rider will certainly be worth considering.

Since the annuity will pay you an income for life, the rider will offer you a higher annual income payment based on your expected shorter life expectancy.

That will not only help you to recover the cost of the annuity more quickly, but it can also provide extra income to help with medical bills and certain treatment options, like home care.

Be sure to do a cost/benefit analysis with your insurance agent to determine if an impaired risk rider will be helpful in your situation.

The Bottom Line – Annuity Rider #7: Impaired Risk Rider

In understanding annuities, the impaired risk rider emerges as a pivotal tool for those with health conditions likely to reduce their longevity.

The rider accelerates income payments, allowing individuals to benefit from higher payments or pay a lower premium based on their health status.

While this may seem counterintuitive in the realm of insurance, the approach factors in a person’s expected shorter lifespan, giving them a financial advantage.

Although only a select number of insurance companies offer this rider due to the unpredictability of modern medical advancements, for those facing health impairments, it presents an opportunity to maximize their annuity benefits, ensuring they receive the financial support tailored to their unique circumstances.