The standard message from the financial community is that Americans are woefully unprepared for retirement. That owes to several factors, one of the major ones being a lack of regular retirement savings contributions. But there may be hope for America’s children, including yours.

One of the most fundamental elements of investing success is starting early and giving your money a chance to grow through compounding earnings. You may be able to help your children do exactly that by opening a Roth IRA for kids.

We all know how important it is to begin investing early in life. But imagine what your kids can do if they begin investing before they graduate from high school.

It’s possible, and a Roth IRA can make it happen. Start by reading this article or researching the best places to open a Roth IRA.

What Is a Roth IRA?

Table of Contents

As the name implies, a Roth IRA is a variation of an individual retirement account. That means you can contribute a portion of your earned income to this account each year. And by doing so, you’ll be building an investment account dedicated primarily toward your retirement. But that said, Roth IRAs can serve other purposes as well, and that’s why they often make sense for children.

This is also a good time to point out that a Roth IRA makes sense for you as a parent too.

Because the investment income earned in a Roth IRA is tax-deferred—and eventually tax-free—there are no tax complications to worry about.

Unlike taxable brokerage accounts and even bank accounts, there’s no possibility of incurring the so-called “kiddie tax” on the investment earnings in a Roth IRA account.

How It Works

In many respects, a Roth IRA works the same as a traditional IRA. You’ll contribute money to the plan out of earned income, and those contributions can earn investment income on a tax-deferred basis.

Funds can be withdrawn from either account beginning at age 59½ without incurring an early withdrawal penalty. Either plan can be invested in an investment account of your choice, including banks, brokerage accounts, robo-advisors, and fund families.

But beyond those basics, Roth IRAs are different from traditional IRAs in the following ways:

- Contributions to a traditional IRA are generally tax-deductible in the year they are made; Roth IRA contributions are not tax-deductible.

- Because they are not tax-deductible, contributions made to a Roth IRA can be withdrawn early without incurring ordinary income tax or the 10% early withdrawal penalty.

- While distributions taken from a traditional IRA after age 59½ are subject to ordinary income tax, distributions made from a Roth IRA will be tax-free if the account has been in existence for at least five years.

- Traditional IRAs are subject to required minimum distributions (RMDs) beginning at age 73; Roth IRAs are not and can literally grow throughout your lifetime.

Point #2 is particularly important when it comes to minor children. If funds are needed to pay for their education, contribution amounts can be withdrawn early without tax consequences. That gives Roth IRAs greater flexibility than traditional IRAs.

Roth IRA Contributions

As is the case with traditional IRAs, the maximum annual contribution that can be made to a Roth IRA is $7,000.

That’s the maximum contribution that can be made (unless you are 50 or older, in which case the maximum is $8,000), but your child can make a smaller contribution.

Remember we said contributions to a Roth IRA are limited to earned income only? That means your child will only be able to contribute from their earned income. If that’s $3,000, that’s fine, and so is $1,000, or even $500.

It isn’t necessary for your child to make the maximum contribution. The primary purpose is to help your child begin saving money for the long term now. That can be accomplished with a few thousand dollars, or with just a few hundred.

Roth IRA Limits for Kids

Once again, we must emphasize that contributions are limited to your child’s earned income. That does not include interest, dividends, gifts, or other sources of income that are unearned.

Contributions can be made up to the amount your child earns from paid work. The best example is a job that reports his or her income on a W-2 each year.

That may come from part-time work or even seasonal employment, like summertime and holiday breaks from school.

But that’s not always the case with minor children. They often earn money from casual work, like babysitting and lawn cutting.

If that’s the case, you’ll need to keep careful records of all money earned, since the people your child performs services for will be unlikely to issue a tax document.

If you have your own business, you may be able to pay your child for performing certain services related to that operation.

For example, if your child runs errands for you, does research, cleans your shop or office, or does typing and filing, you can pay him or her a regular salary for the work.

But if you go this route, go carefully. You can’t pay your child a thousand dollars to do a job that’s only worth $50 on the open market.

You should also be careful about paying your children to do work around the house. While theoretically, this constitutes earned income, proving this to the IRS can be a problem. That strategy works better if your child does similar work for other people too, with you being just another “customer.”

Consult with your tax professional if you have any questions in this area.

Roth IRA Rules

There are very specific Roth IRA rules for minors you need to be aware of. For example, a major limitation of a Roth IRA, or any type of financial account for that matter, is that your child lacks the legal capacity to open the account in his or her own name.

For that reason, a Roth IRA will have to be set up as a custodial IRA in your name, with your child as the beneficiary.

Direct ownership of the account will transfer to your child upon reaching age 18, or whatever the age of majority is in your state of residence.

As an account custodian, you’ll have full authority over the account. That will include deciding where the account is held, and what investments will be made.

On the plus side, it will be possible for you to provide funds for your child to put into a Roth IRA. For example, let’s say your child earns $4,000.

She spends half of it, leaving her with only $2,000 to fund her IRA. But you can contribute the remaining $2,000, so the contribution fully matches her income for the year.

You can also make a contribution for the full amount to your child’s Roth IRA, as long as that amount doesn’t exceed your child’s earned income. Otherwise, there’s no requirement for your child to make a direct contribution to the plan.

Roth IRA Benefits for Kids

There are several good reasons to open a Roth IRA for your minor children.

Having a Solid Financial Foundation for the Future

By starting a Roth IRA for your child as early in life as possible, you’ll be giving him a big head start in life.

That’s best demonstrated with an example:

Let’s say your child makes her first Roth IRA contribution at age 25. We’re going to assume a one-time contribution of $6,000, with a 7% average annual rate of return. By age 65, the account will grow to $89,847.

Now let’s say your child makes her first Roth IRA contribution at age 10. It’s only $3,000, but it will also have an average annual rate of return of 7%. By age 65, the account will grow to $123,945!

Your child will earn an additional $34,000 on the account just by virtue of making a contribution 15 years earlier. And that’s despite the fact that the contribution was only half as large as the one she would make at 25.

Now imagine your child continues to make modest contributions between the ages of 10 and 25—the account balance will grow exponentially. You’ll be giving your child a financial advantage in life that can hardly be matched any other way.

Diverse Use Cases

Obviously, the primary use for a Roth IRA is retirement. But the flexibility of a Roth IRA means it can also be used for other purposes.

As previously discussed, contributions made to a Roth IRA can be withdrawn at any time without incurring tax consequences. That means the money can also be available to help fund your child’s college education.

Because of special IRS provisions regarding IRAs, early withdrawals can be taken for higher education without incurring the 10% early withdrawal penalty.

(Although ordinary income, tax will be imposed on the amount of the withdrawals that represent investment earnings on those contributions.)

That means a Roth IRA is one of the best ways of saving for kids’ tuition. In fact, it’s one of the very best ways to save for kids’ college.

The IRS also allows IRA owners to withdraw up to $10,000 for the purchase of a qualified first-time home purchase. The distribution will be subject to either ordinary income tax on the amount of any accumulated investment earnings or the early withdrawal penalty.

Learning About Money

An underappreciated task for parents is teaching kids about money. In a very real way, learning how to handle money is a survival skill of the first order.

One of the very best ways for your child to learn about money is to begin managing it early in life. No, your minor child cannot directly manage a Roth IRA account—that’s your job. But you can involve them in the process, particularly with investment decisions.

One of the best lessons a child can learn about money is the importance of growing it. Your child will be able to see the account grow through a combination of contributions and investment earnings.

That alone may give your child an incentive to earn money for contributions, but more importantly, to develop a sense of investing for the future.

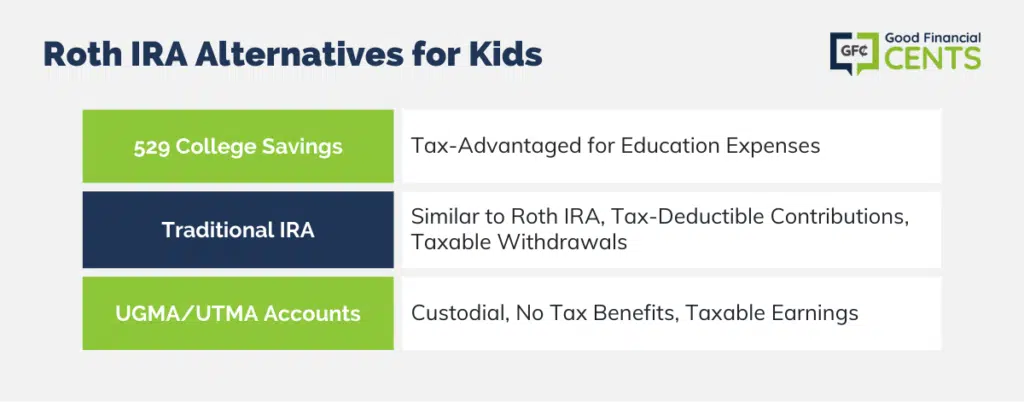

Roth IRA Alternatives for Kids

There are alternative investment accounts to a Roth IRA for kids.

529 College Savings

529 college savings plans are tax-advantaged accounts designed specifically to enable parents to accumulate funds to pay for a child’s college education. Contributions to the plan are not tax-deductible, but the investment earnings accumulate tax-free.

But there is a catch. Investment earnings can be withdrawn tax-free only if the distributions are used to pay for qualified higher education-related expenses. That includes tuition, room and board, books, supplies, and fees.

One of the big advantages of a 529 plan is that you can contribute a lot more money to the plan. Though you can contribute much more on an annual basis, most parents limit contributions to $16,000.

This is the amount the IRS allows you to transfer to your child without incurring the gift tax.

Traditional IRA

A traditional IRA as an investment account compares most closely to a Roth IRA. As previously discussed, there are many similarities.

The contribution limits are the same; they are similarly limited to earned income, the money can be invested any way you like, and investment earnings accumulate on a tax-deferred basis.

The main disadvantage of traditional IRAs is the fact that the contributions themselves are tax deductible.

Because your child is almost certainly in a low or zero tax bracket, it will make little sense to gain a tax break now in exchange for higher taxes when the child is older and earning more money.

Meanwhile, withdrawals made from the plan will be taxable if the contributions are tax-deductible. In either case, the 10% early withdrawal penalty tax will apply.

UGMA/UTMA Accounts

Similar to custodial IRAs, UGMA/UTMA accounts are accounts you set up for the benefit of your child, with you acting as custodian. They can be set up with either a bank or brokerage firm but won’t have tax benefits.

Not only are contributions not tax-deductible, but you will incur tax liability on any investment earnings produced by the accounts.

Summary of the Best Roth IRA for Kids

If you like the idea of having a Roth IRA for your kids—and we hope you do—the next step will be to investigate the best places to open a Roth IRA in 2023.

To get the biggest benefit from a Roth IRA, it’s best to open the plan in an investment-type account, where you can earn dividends and capital gains rather than just low interest in bank accounts.

Some of the best investment firms to consider include the following:

- Betterment: Best Roth IRA for Hands-Off Investing

- M1 Finance: Best for Self-Directed Investing

- Stash: Best for Low Fees

- Fundrise: Best for Real Estate Investing

- E*TRADE: Best Overall

- USAA: Best for Military Families

- Charles Schwab: Best for Low-Cost Investing

- Vanguard: Best for Low-Cost Investing

- Fidelity: Best for Low-Cost Investing

A Roth IRA really is an advantageous program for anyone, but especially for kids. That’s because it offers an opportunity to begin building a financial base early in life. It can mean having extra money available for major expenses in life, like higher education and the first home.