The mortgage industry is incredibly competitive, with hundreds of lenders looking to get your business. But when it comes to VA loans, you don’t want to go with just any lender.

Most lenders don’t do many VA loans, and some do none at all. Since VA loans are a highly specialized mortgage type, it’s best to go with lenders who focus mostly or even entirely on this loan type.

To help you with the decision, we’ve prepared this guide listing what we believe to be the best VA home loans of 2025. We’ll cover each lender, then provide you with a thorough understanding of VA home loans and how they work.

Before we go any deeper, you can scan the comparison table below to get a quick overview of the eight best VA loan lenders of 2025:

Our Picks for the Best VA Loan Lenders February 2024

Table of Contents

We’re not going to keep you waiting – below is our list of what we believe to be the best VA home loans of 2024, and what we believe each is best for:

- Veterans United: Best Overall

- USAA: Best for Lowest Rates

- Quicken Loans: Best Online Lender

- PenFed Credit Union: Best for No Lender Fees

- Navy Federal Credit Union: Best for First-Time Homebuyers

- LendingTree: Best Online Mortgage Marketplace

- Wells Fargo: Best Mortgage and Banking in One Place

- loanDepot: Best for Other Mortgage Options

Best VA Loan Lenders – Company Reviews

Below are summary reviews of each of the eight best VA home loans for 2025. Under each summary review is a link to our full review of each particular lender. Feel free to click through if you’d like more information before making a decision on which VA lender to use.

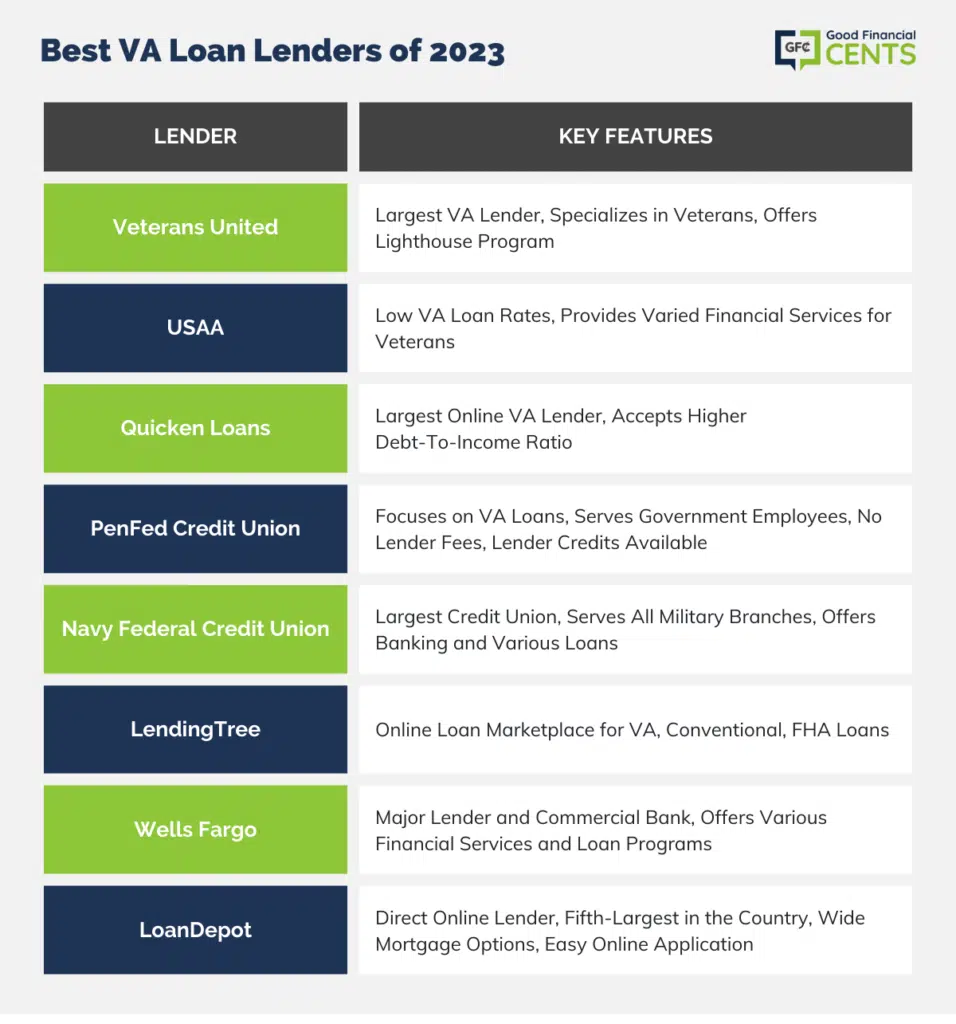

Veterans United takes our top honors as the best overall VA mortgage lender. It’s easy to see why. It’s the largest VA mortgage lender in the country and one that specializes entirely in working with veterans.

For example, the company works with senior members of all branches of the US military, including the Army, Navy, Air Force, and Marine Corps, to help them stay on top of developments affecting veterans. They also offer their Veterans United Lighthouse program.

Not only does it help veterans build and improve their credit, but it also provides a network of real estate agents nationwide who are knowledgeable in VA home purchases.

Why We Like Veterans United: Having the status of the largest VA mortgage lender in the country means veterans are trusting their home financing needs to Veterans United more than any other lender. We also like that the company focuses entirely on VA loans, so they aren’t distracted by other loan programs.

See Our Full Veterans United Review

USAA tends to be on the low end of the interest rate spectrum with VA loans. But there’s a lot more to USAA than just VA loans. It’s a full-service financial provider offering a wealth of financial services designed specifically for veterans. In addition to banking, insurance, and investments, the company specializes in auto insurance, where it consistently ranks at the top of the list for the entire industry.

USAA provides the full range of VA loans, including fixed and adjustable-rate mortgages, as well as jumbo loans. Meanwhile, their USAA Home Learning Center will help educate veterans on the many details of the mortgage lending process.

Why We Like USAA: Not only does USAA provide low rates, but they also offer a wide variety of financial services for veterans. That includes banking, insurance, and investments.

Though it’s not widely known, Quicken Loans is the largest retail mortgage lender in the entire country. But mortgage financing is offered through their online lending portal, Rocket Mortgage. It provides a full range of mortgage products, including conventional and FHA loans, in addition to VA loans. That’s important because if a VA loan is not the best option, Quicken Loans can present alternatives.

Quicken Loans gets our vote as the best online VA mortgage lender. That’s because the entire lending process takes place online, so you can apply and track your progress from the comfort of your home or place of employment. You can also upload most of the required documentation needed for the mortgage application process, right on the website.

Why We Like Quicken Loans: The company website indicates Quicken Loans will accept a debt-to-income ratio (DTI) as high as 60%. This is well above the normal maximum of 43%.

See Our Full Quicken Loans Review

With PenFed Credit Union, short for Pentagon Federal Credit Union, it should be obvious that this lender has a strong orientation toward VA loans. In fact, it mainly provides services for those employed by the US government and its agencies. In addition to mortgages, they also provide auto loans and credit cards. PenFed also offers FHA loans, in case that might be a better choice than a VA loan.

Why We Like PenFed Credit Union: PenFed charges no lender fees, like origination or application fees. The only closing costs you’ll pay will be those charged by third parties, like attorneys, appraisers, and title companies. The credit union also provides up to $2,500 in lender credits, which can be used toward third-party closing costs and other expenses.

See Our Full PenFed Credit Union Review

Navy Federal Credit Union is the largest credit union in the United States, and by a very wide margin. And although the name includes “Navy,” they welcome members of all other branches of the US Armed Forces. At the credit union, you can take advantage of banking services, like deposit accounts, auto loans, and credit cards, in addition to home mortgages.

Navy Federal also provides conventional and FHA loans, in addition to VA loans.

Why We Like Navy Federal Credit Union: The fact that this lender is a credit union, and one that caters to military families, makes it a top choice for first-time homebuyers.

See Our Full Navy Federal Credit Union Review

LendingTree is an online loan marketplace, where dozens of lenders offer their loan programs to consumers. Not only does it include mortgages, but you can also find car loans, credit cards, personal loans, and other financial products on the platform. LendingTree is not a direct lender, but the website is free to use.

Of course, the advantage of shopping on an online marketplace is that you can also consider other financing options. In addition to VA loans, participating lenders also offer conventional and FHA loans.

Why We Like LendingTree: It’s an excellent choice for anyone who is primarily shopping for the lowest mortgage rate. By completing a simple online loan application, you’ll get offers from multiple lenders. You can then choose the lender that offers the best combination of rates and terms.

See Our Full LendingTree Review

Wells Fargo is not only one of the largest mortgage lenders in the country but also one of the very biggest commercial banks. That means you can enjoy full-service banking, including checking, savings, CDs, access to a wide variety of loan programs, and even small business banking – with the same company you get your mortgage from.

Wells Fargo provides all types of mortgage financing, including conventional and FHA loans, as well as VA mortgages. And as a bank, they also offer secondary financing, including home equity loans and home equity lines of credit (HELOCs). Eligible VA borrowers should also be aware that Wells Fargo does not charge an origination fee on VA loans.

Why We Like Wells Fargo: Full-service bank that can accommodate all your financial needs, including small business banking if you are self-employed.

See Our Full Wells Fargo Review

loanDepot is a direct lender that, much like Quicken Loans, operates entirely online. That will make for an easy and convenient loan process, including the ability to upload required supporting documentation, right on the website.

loanDept is a direct lender, so you can be confident you will be working with them through the entire mortgage process. The company operates in all 50 states, as well as Washington, DC. Though it’s not as well-known as some of the other lenders on this list, it’s actually the fifth-largest mortgage lender in the country.

Why We Like loanDepot: They offer the full range of mortgage financing products, including conventional and FHA loans, as well as secondary financing options, in addition to VA mortgages.

VA Home Loan Guide

How Does a VA Loan Work?

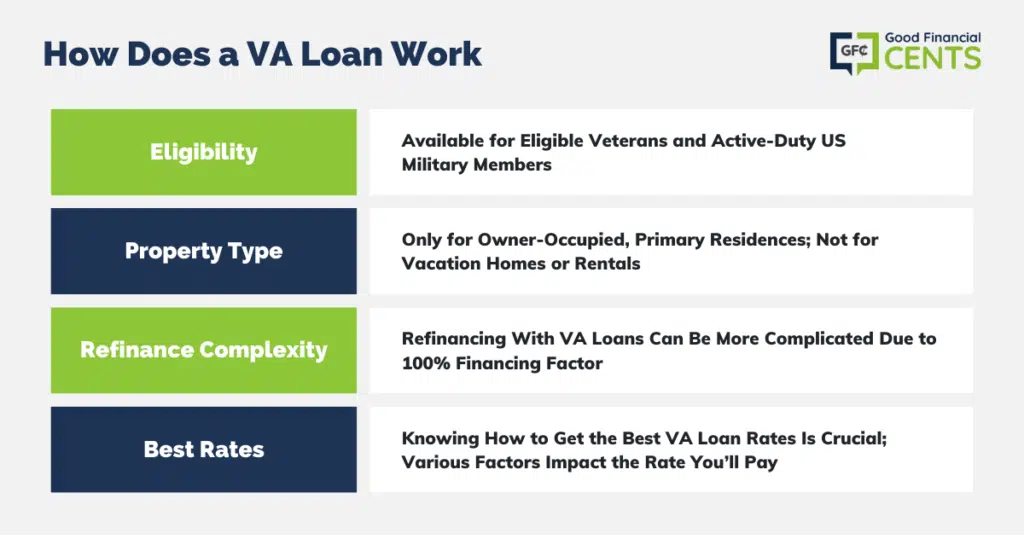

In most respects, VA loans work like any other type of mortgage, including conventional and FHA loans. The main difference is that you must be an eligible veteran or an active-duty member of the US military to qualify for a VA loan.

You should also be aware that VA loans are only available for owner-occupied, primary residences. If you want to purchase a vacation home or rental property, you’ll need to consider a conventional loan instead.

Probably the biggest advantage of VA loans is that they provide 100% financing. Not only will that eliminate the need for a down payment, but also for a second mortgage or a home equity line of credit (HELOC).

Though HELOCs have become common for homeowners, it’s always best to understand the pros and cons of a HELOC. Though they have definite advantages, there are certain risks. Either way, they’re usually not necessary if you qualify for a VA loan.

VA loans are available for both purchases and refinances. Rates and fees are lower when you do an Interest Rate Reduction Refinance Loan (IRRRL), as opposed to a cash-out refinance. It’s important to understand when to refinance, then to work with the best mortgage refinance companies for VA loans.

Because of the 100% financing factor, refinances can be more complicated with VA loans than with conventional loans.

Whether you are purchasing or refinancing, it’s important to know how to get the best VA loan rates. Under “How to Qualify for a VA Loan” below, we’ll go over the factors that will affect the rate you’ll pay.

What Is the VA Funding Fee?

When you make a down payment of less than 20% using a conventional mortgage, you’ll be required to pay what’s known as private mortgage insurance, or PMI. This is an insurance policy, you as the homeowner, are required to purchase to partially compensate the mortgage lender should you default on the loan.

VA mortgages do not use PMI. Instead, they have what is referred to as the VA funding fee. This is a fee collected by the Veterans Administration, which will partially compensate lenders for borrower default on the loan. This is especially important with VA loans since they involve 100% financing.

The VA funding fee is paid at the time of closing. If it isn’t paid by the property seller, lender, or a gift from a family member of the borrower, it will be added to the loan amount. This is the most common scenario.

For example, on most purchases, the funding fee will be 2.3%. If the loan amount is $300,000, the amount owed will be $306,900, with the VA funding fee added to the principal amount of the loan. The borrower will then effectively pay the funding fee over the life of the mortgage.

There are various rates that apply to the VA funding fee. Those rates are as follows for 2025:

| If Your Down Payment Is… | Your VA Funding Fee Will Be… | |

| First Use | Less Than 5% | 2.15% |

| 5% or More | 1.5% | |

| 10% or More | 1.25% | |

| After First Use | Less Than 5% | 3.3% |

| 5% or More | 1.5% | |

| 10% or More | 1.25% |

Note:

The VA funding fee is different for refinances. If you are doing an Interest Rate Reduction Refinancing Loan (IRRRL), in which you are refinancing only to lower the interest rate and payment on your loan, the fee is 0.5%.

If you are doing a refinance and taking cash out with the loan, the VA funding fee will be 3.6%.

Just for comparison’s sake, conventional mortgages charge monthly mortgage insurance premiums, which VA loans don’t have. FHA loans have both upfront and monthly premiums.

If you do have to add the VA funding fee to your loan amount, think of it as one of the costs of owning a home. When it comes to VA loans, the funding fee is a big reason why you’ll qualify for the loan.

Pros and Cons of a VA loan

What Is the VA Loan Limit?

For 2025, the standard maximum VA loan amount is $766,550 for a single-family property. However, in areas designated as “high cost,” the maximum loan amount can be as high as $970,800. The maximum limits are higher for owner-occupied homes with 2-4 living units in them.

But even if you want to purchase a home for more than the standard maximum, you can do so using the VA Jumbo program. That’s a program that enables you to buy a higher-priced home, but it will require you to make a partial down payment.

It works like this: Let’s say you want to purchase a home for $926,200. That’s $200,000 above the standard maximum loan limit.

If you only needed to borrow the maximum of $766,550, you could do so with no down payment whatsoever. But under the VA Jumbo Loan Program, you’ll be required to make a down payment equal to 25% of the amount by which the loan exceeds the standard maximum.

Since the property you are purchasing is priced $200,000 over the standard maximum limit, you’ll need to make a down payment equal to $50,000, which is 25% of $200,000.

That may seem like a big chunk of money. But $50,000 represents a down payment of just under 6% on a home worth $926,200.

That’s an outstanding deal since conventional Jumbo loans typically require a 20% down payment.

How to Qualify for a VA Loan?

To be eligible for a VA loan, you must be either an active-duty member of the US military or an eligible veteran. Eligibility is determined by acquiring a VA Certificate of Eligibility (COE). You may have received this certificate upon discharge from the military, but don’t worry if you didn’t. Your mortgage lender will assist you in obtaining the certificate.

Whether you are a veteran or currently on active duty, there are specific requirements for that eligibility based on when you served and for how long. Eligibility will not be granted if you were dishonorably discharged.

Apart from VA eligibility, you can qualify for a VA loan the same way you would with any other mortgage program. While the following information will help you understand the process, it’s best to let a lender show you how to get approved for a home loan.

Other Considerations Your Lender Will Look At

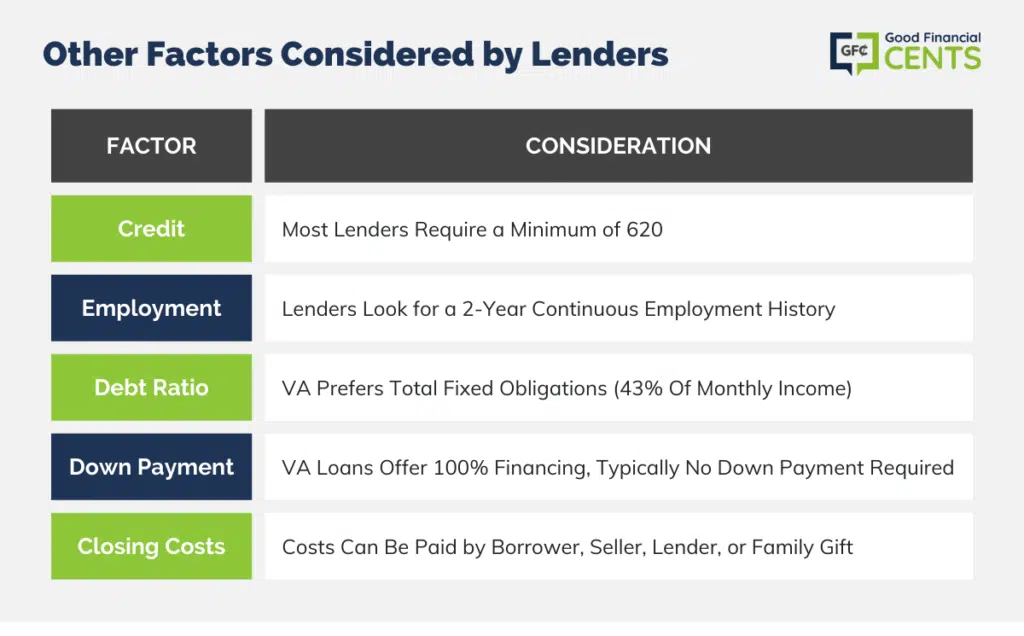

Credit

The Veterans Administration does not set a specific minimum credit score, but rather leaves it up to individual lenders. Most lenders set the minimum score at 620, though some will go lower. The lender will also consider individual components of your credit, such as any history of bankruptcy, foreclosure, or serious delinquencies.

Just as is the case with other types of mortgages, your credit will have a strong impact on the rate you’ll pay on your loan. Be sure to check current mortgage rates based on your current credit score.

Employment

Lenders will generally look for a continuous employment history of at least two years. Military service or college can partially or entirely satisfy this requirement, as long as you have the promise of employment in a job related to your military or college experience.

Debt Ratio

VA generally prefers your total fixed obligations, including both the new housing payment and any recurring debt payments, to be within 43% of your stable monthly income. However, lenders will sometimes go higher if you have compensating factors, like a down payment, cash reserves after closing, or excellent credit.Your debt ratio will be a major factor in answering the question, How much house can I afford?

Your debt ratio will be a major factor in answering the question, How much house can I afford?

Down Payment

Since VA loans are famous for providing 100% financing, a down payment is typically not required.

Closing Costs

These can be paid by the borrower, but also by the seller, the lender, or a gift from a family member.

Types of VA Loans Available

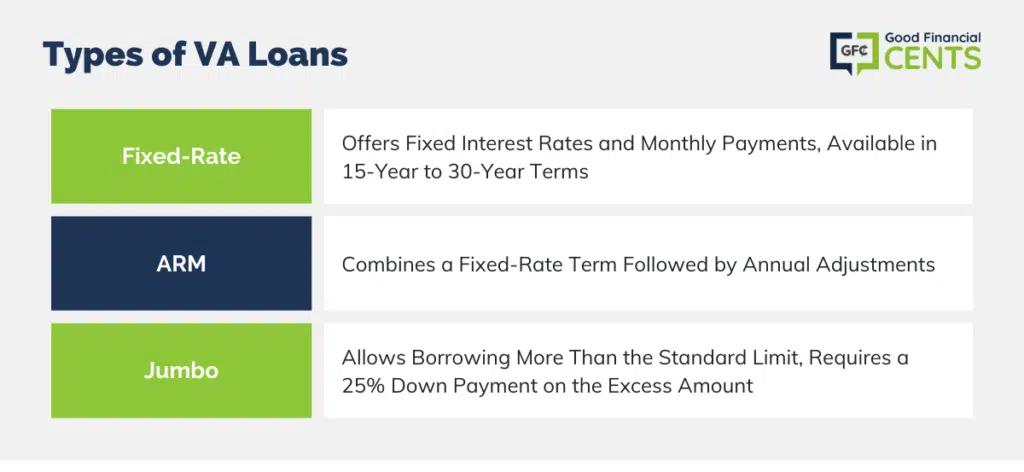

VA loans are available in three basic types, fixed-rate, adjustable-rate (ARM), and Jumbo loans.

Fixed-Rate

These are mortgages with terms ranging from 15 years to 30 years and carry a fixed rate and monthly payment. Though the interest rate on a fixed rate is higher than it will be for an ARM, it’s a much less risky loan since the payment will never change. This will be particularly important if interest rates rise in the future.

Before choosing a 15-year loan, which has a higher monthly payment, you should first consider the implications of a 15-year vs 30-year mortgage. For most borrowers, the 30-year loan will offer a lower payment, which will be a more comfortable fit.

ARM

This loan type has a fixed-rate term, which is followed by annual adjustments. For example, with a 5/1 ARM, you’ll have a fixed rate for the first five years of the loan. After that, the rate will change each year. To keep the payments from going too high upon adjustment, ARMs have rate caps.

For example, in a typical arrangement, the rate will not be able to increase more than 2% on the first adjustment. Subsequent adjustments will similarly be limited to 2%, with a maximum adjustment of 5% over the life of the loan.

However, even with the rate caps, your rate and payment can go up substantially from the initial term. If the loan starts at 4% and has a 5% lifetime cap, you may eventually end up paying 9%. These loans are suitable only if you plan to stay in the home for no more than the initial fixed-rate term of the program.

Jumbo Loans

We covered this earlier under “What is the VA loan limit,” so we won’t go into any detail here. A VA Jumbo loan is simply a program that enables an eligible borrower to borrow more than the standard loan amount, in exchange for making a down payment equal to 25% of the excess loan amount. Before taking a jumbo loan, be sure to gain a thorough understanding of the VA Jumbo loan. The higher dollar amount does represent a greater risk.

How We Found the Best VA Loan Lenders

There are many mortgage lenders offering VA loans, but only a small percentage specialize in this loan type. To come up with our list of the eight best VA loans for 2025, we considered the following criteria:

The number of VA loans the lender does.

- Specialization in VA loans.

- The number of VA loan programs the lender offers.

- The lender’s reputation.

- Specializations, like accommodating low credit scores, low closing costs, and other services offered by the lender.

In addition, we chose lenders that cover wide geographic areas to benefit as many people as possible.

Summary of the Best VA Home Loans of August 2024

- Veterans United: Best Overall

- USAA: Best for Lowest Rates

- Quicken Loans: Best Online Lender

- PenFed Credit Union: Best for No Lender Fees

- Navy Federal Credit Union: Best for First-Time Homebuyers

- LendingTree: Best Online Mortgage Marketplace

- Wells Fargo: Best Mortgage and Banking in One Place

- loanDepot: Best for Other Mortgage Options

We believe any one of these lenders will be an excellent choice to provide you with a VA loan.

Final Thoughts – 8 Best VA Loan Lenders of 2024

Selecting specialized VA loan lenders is vital in the competitive mortgage market. This guide highlights top choices: Veterans United for veterans, USAA for low rates, Quicken Loans for online convenience, PenFed Credit Union for no fees, Navy Federal Credit Union for first-time buyers, LendingTree for online comparisons, Wells Fargo for banking integration, and loanDepot for diverse options.

Each lender addresses unique needs, offering tailored solutions for VA loans in 2025.