I’m sick of cash savings rates. Big banks at 0.06%? No thanks. Even the best online savings accounts are only hovering around a minuscule 1%.

Where can I get a decent savings rate anymore? If you’re a holder of cryptocurrencies like bitcoin, possibly in a cryptocurrency savings account, where some accounts are paying well over 5%!

Table of Contents

Yes, you read that correctly.

Wait, Isn’t Cryptocurrency Super Risky?

Yes, Bitcoin, Ethereum, and other cryptocurrencies are very volatile, making them very hard to hold long-term. For example, this year alone bitcoin has traded down to $3,000 and as high as $12,500! Please, please, please do NOT go out and buy Bitcoin just to try and earn interest on it. Most cryptocurrencies are WAY too volatile.

However, there are various “stable” currencies that trade on a 1-to-1 basis with the US dollar. These are the currencies we want to hold and earn interest on. Even though these currencies are pegged to the US dollar (i.e. 1 stablecoin = $1 USD), this doesn’t mean that you have no risk. Market forces can make a stable coin worth less than a dollar, in a similar way to how money market funds have occasionally “broken the buck.”

All of this is to say: that just because this account has the words “savings account” next to it, doesn’t mean it’s the same as an FDIC, U.S. dollar savings account at a regulated bank. You need to ultimately decide if the risk is worth the potential returns on a very liquid asset. Here’s how I’m thinking about this new class of accounts.

How to Earn 5%+ in a Crypto Savings Account

Decide How Much Money to Try

As I laid out in my Barbell Investing article, I’m hugely risk averse. I’m leery of “too good to be true” promises, so I run many small experiments where I can learn by doing. This is no different.

I opened the accounts to figure out what I needed to know to decide if I should add more money. I first invested in bitcoin (BTC) in 2014, so I was relatively early and had built up a sizable portfolio of crypto assets over the last six years. I chose to make an initial deposit of $2,000 mainly because I had $2,000 of USDC (Stablecoin) idly sitting in my Coinbase account.

If you don’t already own cryptocurrency, you’ll choose a dollar amount (for those in the US) that you’re comfortable with. There are generally no minimum deposit or minimum balance requirements; however, some services have minimum withdrawal requirements.

Open a Crypto Savings Account

Coinbase is one of many options. They have a wide range of coins available and competitive deposit rates. Setting up your account is a breeze, and they use the same bank-level encryption that every other financial institution uses.

Choose Which Currency You Want to Hold

Once you have stablecoin or cryptocurrency in your account, you can trade into any of the other available currencies. For the purpose here, I don’t recommend trading cryptocurrencies. Remember, I’m after as stable of a return as I can get that closely mimics a normal savings account, but with a higher return.

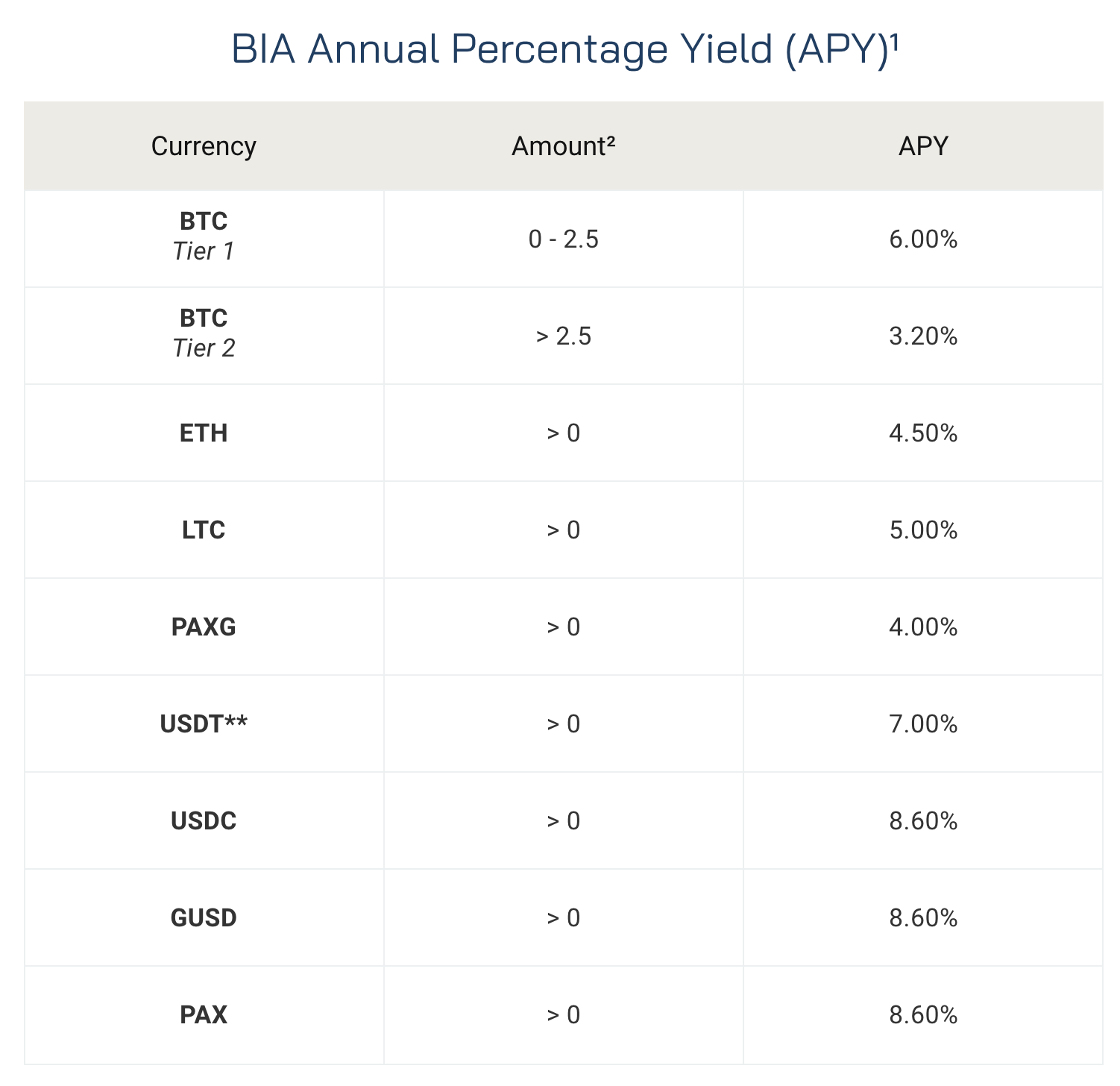

Also, the stablecoins offer the highest interest rates as you can see here:

I chose USDC as my preferred currency simply because I already owned some. I don’t know enough about the differences in these stable coins to recommend one over the other at this time.

Start Earning

Once you’ve deposited money in your account, you don’t need to do anything else. Interest will accrue daily, and is deposited in your account monthly. It’ll look something like this:

Understand How Crypto Savings Differs From Cash Savings

To take this beyond an experiment, we really need to know what the overall risk is here. Your cash currency is protected in several ways that cryptocurrency isn’t.

- First, your savings account is FDIC-insured, so you don’t lose your money if your bank becomes insolvent.

- Second, the U.S. dollar is a world reserve currency backed by the full faith and credit of the U.S. government, whereas the U.S. government doesn’t back any of these stablecoins — YET.

- Third, a stable coin pegged to the U.S. dollar isn’t the same as a dollar. See here about Tether’s peg.

- Fourth, big banks have billions to throw at security. A cryptocurrency upstart might fall short on some security measures. I honestly don’t know how to analyze this at the moment.

Decide to Go Bigger

Understanding the above risks, I don’t think it makes sense to have a gigantic amount of money in these accounts yet. Further, I wouldn’t suggest putting your emergency fund money in an account like this, or any money that you think you can’t live without.

The risk of losing money is unlikely, but it’s non-zero, and it’s absolutely higher than the risk of losing your cash savings account money. But is it worth the risk anyway?

To me, it is — on a portion of my liquid assets. It makes sense for me to go bigger and add more to my account because I’m not risking my emergency fund and I was already taking many of the risks above by holding USDT in another account without getting paid for it like I am now.

Does a Crypto Savings Account Make Good Financial Cents?

For now, this experiment makes sense for people who are long-term cryptocurrency holders, or people looking to juice their rate of return on liquid assets. However, because of the additional risks outlined above, it doesn’t make sense to put a huge amount of your savings in one of these accounts.

What would I need to see to change my mind?

I would put a significant amount of money behind this account if my principal was insured against loss and theft in similar ways to the US banking system.

Basically, if I could insure my account against devaluation, theft, and insolvency — at say, 2% per year — I’d borrow millions of dollars to add to this account and earn a very healthy low-risk spread. This is the definition of a carry trade.

Leave a Reply