One million dollars seems like a lot for a life insurance policy. Well, if that seems like a lot, I can only assume that a $3 to $4 million policy seems outrageous.

But the fact remains these types of policies exist for a reason. There are situations where high-income earners or those looking to protect their estate would need such a large insurance policy.

So, who would need a 3 million-dollar policy, and how much should you need? Let me give you a quick example…

How Much Life Insurance Do You Need?

Most financial experts suggest that you need 10 to 15 times your income in life insurance coverage. So if a high-income earner was making $200,000 per year x 15 – that would get you to the $3 million dollar mark of coverage needed.

Even someone making $250,000 would be in that ballpark of $2.5 million to $3 million of life insurance.

If you’re not really sure how much you need and would rather base it on your total household needs, you can also try out a life insurance calculator that will get you a more specific amount.

Either way, the main goal of purchasing any life insurance policy is to protect your family decades into the future.

You may only need a 10-year term policy, but if you’re younger, I would highly suggest considering at least a 20-year term or a 30-year term if it’s not cost-prohibitive.

I will also add having a $3 million-dollar policy is nothing to flex on.

In most situations, buying a term life policy makes the most financial sense so that you can invest more towards building wealth.

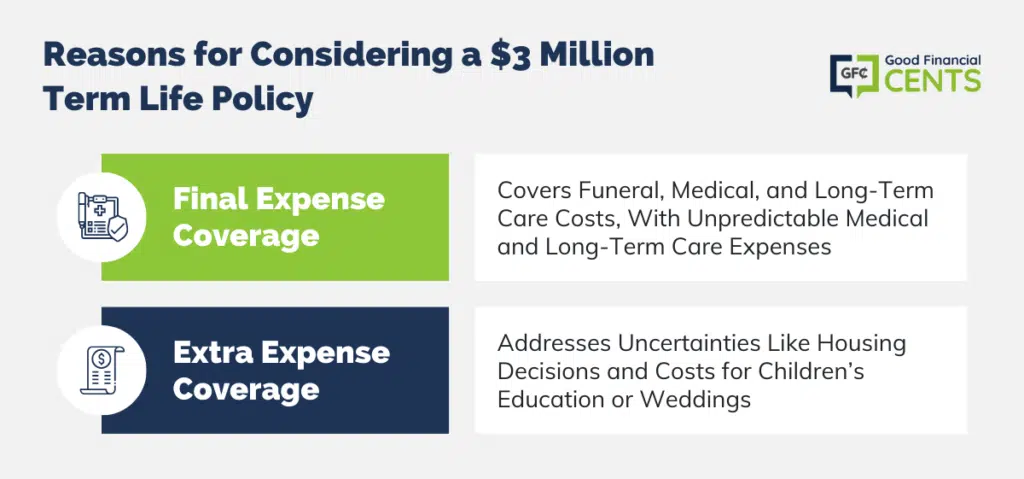

Reasons You Might Need a $3 Million Term Life Policy

We’ve already talked about the importance of asset protection and why you may need to purchase such a large life insurance policy for yourself. Here are a few other examples of why someone may want to consider this type of policy:

- Final Expense Coverage: Final expenses are exactly how they sound. This is to cover funeral costs and medical bills and possibly to cover long-term care expenses where there is no insurance coverage to help out.

- Extra Expense Coverage: This is the complete unknown. Will your family be able to stay in your current home, or will they be more comfortable moving out of state to be closer to family? And if you have kids, there’s a variety of costs to consider, anything from college tuition to helping them pay for a wedding.

With so many unknowns, it’s important to have a serious conversation about all of the things that could be or should be considered. And if you’re not confident that you’ll be able to uncover all of the important considerations, this is where a financial professional or independent life insurance agent can help out.

How Much Will a $3 Million Life Insurance Policy Cost?

Here are some sample rates so you can get an idea of how much this type of policy will cost.

| Age | Gender | Term | Amount | Premium |

|---|---|---|---|---|

| 30 | Male | 30 years | $3 million | $173.49 |

| Female | 30 years | $3 million | $133.69 | |

| 35 | Male | 20 years | $3 million | $95.47 |

| Female | 20 years | $3 million | $81.29 | |

| 40 | Male | 15 years | $3 million | $106.49 |

| Female | 15 years | $3 million | $92.49 | |

| 45 | Male | 10 years | $3 million | $138.17 |

| Female | 10 years | $3 million | $118.46 |

Here are some more rates from a different company for a non-smoking male.

| Age | Face Value | Premium |

|---|---|---|

| 30 | $3 million | $99 |

| 40 | $3 million | $150 |

| 50 | $3 million | $431 |

| 60 | $3 million | $1,231 |

| 70 | $3 million | $4,654 |

| 80 | $3 million | $14,138 |

Both of the tables above are for illustrative purposes. A variety of factors will determine what the actual cost will be.

Underwriting a $3 Million Term Life Insurance Policy

The underwriting process of obtaining a $3 million policy is no different than getting any other type of insurance policy.

When I took out my $2.5 million policy, I scheduled an appointment for a nurse to come to my office for the paramedic exam. This is the basic exam where they collect your height, weight, blood pressure, and any other pre-existing conditions. They also take a small blood and urine sample, which then gets delivered to a lab for further testing.

The whole process is fairly seamless, and they are more than willing to work around your schedule.

Financial Requirements for a $3 Million Policy

You may think that a life insurance company will happily take your money if you’re willing to pay for a 3 million-dollar policy. That is actually not the case. Far from it, actually.

First, you’ll have to verify your income. Any life insurance company is going to be suspicious of an individual who is applying for a million-dollar + policy that is only making an income of $25,000 per year.

The common-sense rule applies here, and it just doesn’t make sense.

Another thing to consider is that the younger you are, the more likely you are to get approved for life insurance, including larger policies.

Previously, we discussed how most financial experts suggest getting between 10x to 15x your income amount as life insurance coverage, but most companies will have a maximum amount of coverage depending on your age.

Below is a sample table of what this may look like depending on your age and how much you are making.

| Age Range | Income Coverage Maximum* |

|---|---|

| 18 – 29 | 35x |

| 30 – 39 | 35x |

| 40 – 49 | 25x |

| 50 – 59 | 20x |

| 60 – 65 | 15x |

| 66 – 74 | 10x |

| 75 – 79 | 5x |

| 80+ | Varies by Carrier |

*Multiply by this time your gross income (before taxes)

Laddering Your $3 Million Policy

If you’re familiar with the concept of laddering your CDs or bonds, laddering (or layering) a life insurance policy is very similar. The difference here is that not locking your money in for a long time actually helps more with cost. Let me explain…

Let’s say, for example, that you are a 35-year-old corporate executive with three kids and a healthy mortgage. You and your wife have had lengthy discussions, and after meeting with a financial professional, you have decided that $3 million dollars of coverage is the appropriate amount that you need.

You may have the income to pay for a $3 million policy in a 30-year term, but you also know your home should be pretty much paid off in 20 years, and you might be wondering if you really need the 30-year policy.

In this situation, you may decide to take out a $2 million-dollar policy for 30 years and simultaneously take out a second million-dollar 20-year term policy.

This way, you have the $3 million of protection until your home is paid off and your kids are out of college. once that is done, you still have coverage for another 10 years, are you don’t have to pay on the second policy anymore.

Can You Qualify for Certain Health Conditions?

When seeking life insurance coverage, there are several factors that will affect the cost and whether you get approved. Another big factor is the life insurance company. What most consumers don’t understand is that if two different people with the same health conditions were to apply at two different insurance carriers, the cost and whether or not they get approved could be totally different.

The above is assuming that both individuals are in good health. What happens if there are health concerns? Or if there is a family history of pre-existing conditions such as prostate cancer or heart disease?

These types of high-risk conditions will have a dramatic impact on how much you have to pay and whether the insurance company is willing to provide coverage.

High-Risk Condition Case Study

Years ago, I was working with a male in their mid-70s who was 4 years removed from having open-heart surgery. He had been following his doctor’s orders of maintaining a healthy weight, eating healthy, exercising, and taking all of the prescribed medication he was given.

Enough time had passed, and he was comfortable trying to seek affordable life insurance. However, he began the process and was frustrated because he kept getting denied. He almost gave up, but after contacting a few other carriers, he was finally able to get the coverage that he needed.

The lesson learned here is to never give up. Remember “your why” in seeking life insurance coverage. If it’s for your family, then do whatever it takes to get coverage. It’s also helpful to seek assistance from a qualified independent life insurance agent who is experienced in helping people with high-risk conditions get approved.

Other factors that will affect your getting approved for life insurance coverage are the following: age, gender, health history, family health history, occupation, hobbies, drinking, smoking, and weight.

The Bottom Line – How to Buy a $3 Million Life Insurance Policy

Securing a $3 million life insurance policy involves careful consideration of income, family needs, and future expenses. Experts recommend coverage of 10 to 15 times one’s income. While costs vary based on factors like age and gender, policy laddering can optimize coverage duration.

Underwriting involves medical exams and financial verification. Health conditions and carrier selection play significant roles in approval and cost. It’s vital to persist in seeking coverage, especially for high-risk cases. Ultimately, a well-structured life insurance policy safeguards family finances and provides peace of mind for the uncertain future.