If you have an enlarged heart due to left ventricular hypertrophy, it’s going to be an issue for life insurance. Insurers will see this condition and worry that it could lead to more serious heart problems in the future. You may still be able to get insurance coverage, though, especially if you put together a well-planned application.

To help you get ready, we’ve put together a guide to the underwriting standards for someone with an enlarged heart due to left ventricular hypertrophy.

Table of Contents

- Life Insurance Underwriting With an Enlarged Heart

- Understanding the Implications of an Enlarged Heart on Life Insurance

- Life Insurance Quotes With an Enlarged Heart

- Enlarged Heart Life Insurance Case Studies

- Working With an Independent Insurance Agent

- The Bottom Line – Life Insurance With Enlarged Heart

Life Insurance Underwriting With an Enlarged Heart

During the application process, the agents are going to ask you about a hundred questions about your health. Some of those questions are going to focus on your enlarged heart:

- When were you diagnosed with an enlarged heart?

- What caused the left ventricular hypertrophy?

- What is your CT ratio, and what is the thickness of your left ventricular wall?

- Did you ever have surgery to treat your condition?

- Do you have a family history of heart disease?

- Do you have any other risk factors for heart disease?

- What medications are you taking?

Common prescriptions for an enlarged heart include Beta-blockers, Nitrates, ACE inhibitors, Statins, and Diuretics. None of these medications will cause you to be declined for life insurance, depending on your condition.

As you complete your application, answer in complete detail. This is your chance to show the underwriter that your heart condition is under control. Also, if your application seems incomplete, the underwriter could decline your policy or give you a bad rating.

Understanding the Implications of an Enlarged Heart on Life Insurance

An enlarged heart on its own isn’t fatal. However, it presents a significant concern for life insurance companies. This is because the condition often leads to heart failure, as the heart has to work harder due to hypertrophy.

The root causes for an enlarged heart typically include high blood pressure or heart disease, both of which are problematic for insurers. In some rare instances, genetics or excessive exercise can lead to this condition.

As part of their evaluation, underwriters will delve deep to understand the severity of your left ventricular hypertrophy and ascertain if other health issues exist.

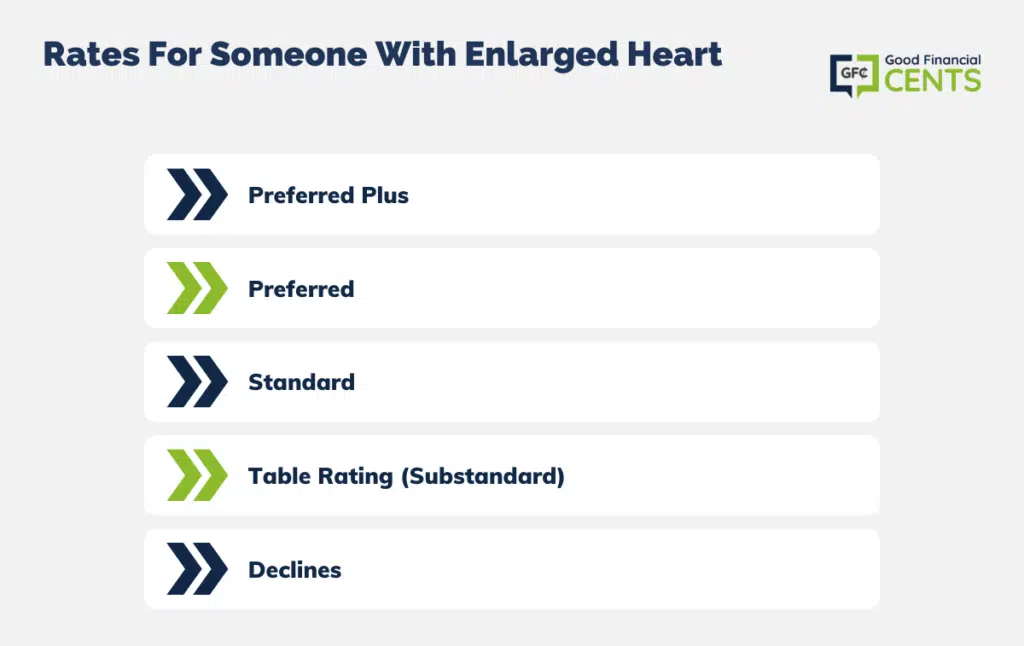

Life Insurance Quotes With an Enlarged Heart

Every insurance company categorizes applicants into various rating groups based on their health condition and associated risks:

- Preferred Plus: Generally impossible. An enlarged heart comes across as too much of a potential health risk for an applicant to get the best insurance rating.

- Preferred: Possible in very rare cases. The applicant must be in great health or have no other health risks for heart disease. Applicants who have an enlarged heart from exercise or genetics are more likely to receive this rating than applicants who have an enlarged heart from high blood pressure.

- Standard: Most likely for an applicant with an enlarged heart. The applicant’s CT Ratio should be below 53% with a left ventricular wall no thicker than 13 mm. Applicant should also be in decent health and not have any serious risk factors for heart disease.

- Table Rating (substandard): Most applicants have an enlarged heart. The rating will depend on the applicant’s CT ratio, ventricular wall thickness, whether the applicant needed surgery, and whether the applicant has other risk factors for heart disease.

- Declines: Applicants with severe hypertrophy, a ventricular wall thicker than 17 mm. Also, applicants with a CT ratio over 57% or with other strong risk factors.

Enlarged Heart Life Insurance Case Studies

Your life insurance application can make a big difference when you apply with an enlarged heart. To help you understand all of this, here are a few stories about past clients.

Case Study #1: Male, 66 y/o, diagnosed with an enlarged heart at 63, caused by high blood pressure, former smoker, taking Beta Blockers and Ace Inhibitors,

This applicant had high blood pressure for several years and didn’t do enough to treat this issue. It eventually led to left ventricular hypertrophy at 63. He also smoked, which certainly wasn’t helping his heart.

At this point, the applicant turned things around. He started taking medication to treat his blood pressure, quit smoking, and started exercising. This helped his health, even if he still had to deal with an enlarged heart.

He could only receive extremely expensive policies. We believed that insurance companies were not giving enough credit to his lifestyle improvements.

We recommended he see his doctor and get a note vouching for his improved health and better lifestyle. After he did this, he was able to qualify for a standard rating plan.

Case Study #2: Female, 58 y/o, diagnosed with an enlarged heart at 56 due to genetics, otherwise in great health.

This applicant was in near-perfect health when she was diagnosed with an enlarged heart at 56. This was a case of bad luck and genetics rather than a sign of heart disease. However, when this client tried to get life insurance, she only received rated policies.

We suggested she get an EKG to test the strength of her heart. The test showed she was in good health and had no complications due to her condition. By reapplying, she got a discounted preferred rating.

An enlarged heart doesn’t have to get in the way of life insurance coverage. By following this advice, you can give yourself the best possible chance of getting insurance at an affordable rate.

Working With an Independent Insurance Agent

To get affordable life insurance, you need to work with one of our independent insurance agents. We can help you compare dozens of highly rated companies across the nation, which means that we can bring all of the lowest insurance rates directly to you. Every company is going to view an enlarged heart differently.

Some insurance companies are going to view your diagnosis more favorably than other companies, which means that they will give you much lower rates. Some companies have better rates for anyone with a high-risk problem, like an enlarged heart. You’ll need to do some shopping around to find one that offers you cheaper coverage.

Aside from bringing you the lowest premium rates, we are here to help you decide which kind of policy is going to meet your needs. It can be difficult and confusing trying to decide between the different kinds of plans, but it shows you which company will give your family the perfect protection.

If something tragic happens to you, your debts are going straight to your family. Your life insurance will help your family pay off those debts. That’s not the inheritance you want to leave behind to your loved ones.

The Bottom Line – Life Insurance With Enlarged Heart

Securing life insurance with an enlarged heart due to left ventricular hypertrophy may seem challenging, but with the right approach and thorough preparation, it’s feasible. It’s essential to provide complete and detailed information during the application process, showcasing that your heart condition is well-managed.

By understanding the underwriting standards and potential ratings you might receive, you can set realistic expectations. Furthermore, the case studies highlight the importance of persistence and proactive measures in obtaining favorable terms.

Working with an independent insurance agent can be invaluable, guiding you to companies that view your condition most favorably. Remember, your life insurance isn’t just for you; it’s a safety net for your loved ones, ensuring they are protected financially in your absence.