When you decide that you are going to roll over a retirement plan from a previous employer into a Roth IRA, what’s the best place to do that? Albert R. asks that exact question from Ask GFC:

“Can I roll over my 401k to a Roth IRA when I quit my job? If so, which is the best place to roll it over at, my Credit Union or a place like Vanguard?” – Albert R.

The choice of where to invest your Roth IRA is the second most important decision in the conversion process – after the decision to do it at all. Albert mentions his credit union or Vanguard, and we’ll take a look at both, plus some other possibilities.

Table of Contents

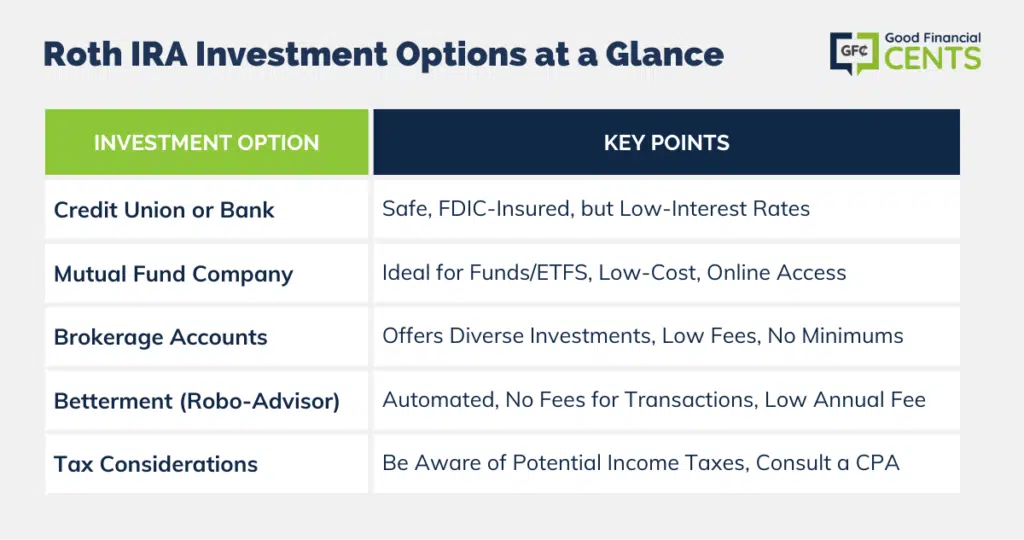

Credit Union or Bank

Albert mentions his credit union as one of the options for the 401(k) rollover. I’m also going to address banks in this section because they are so similar to credit unions.

This is an incredibly safe option, since money saved at credit unions and banks is not subject to market fluctuations. Your accounts are also covered by FDIC insurance for up to $250,000 per account, per depositor. They are just about the safest places to invest money if you don’t want to risk losing money.

But it all goes downhill from there. Credit unions and bank investments are interest-bearing, and interest rates are simply too low right now to work for long-term investment plans, such as retirement accounts.

A certificate of deposit paying 1% interest simply can’t keep up with a 2% rate of inflation. It means that you will be losing 1% of your investment each and every year. You may only lose it slowly, but you will lose it. And that defeats the whole purpose of saving money for retirement in the first place.

Credit unions and banks are excellent if the preservation of capital is your only purpose. That is certainly not the case when it comes to retirement savings. You have to grow it, and these institutions are not the place to do that.

Mutual Fund Company – Like Vanguard

If you only plan to invest in mutual funds and Exchange Traded Funds (ETFs), and not individual stocks or other types of investments, it’s often best to go directly to the source, which is an actual mutual fund company. They do funds and only funds, and can often provide them at lower fees. Some examples included Fidelity and T. Rowe Price.

Albert specifically mentions Vanguard as a possible trustee for his Roth IRA rollover, and I agree that it would be a good choice. Vanguard is one of the very best mutual fund companies, offering both easy online account access and some of the lowest-cost funds available. In fact, Vanguard is actually a non-profit trustee dedicated to providing its customers with some of the lowest investment fees in the industry.

Vanguard has no account fees for a Roth IRA, as long as you access online statements and confirmations (they do charge $20 for paper documents).

You can open an account with as little as $1,000 for their starter mutual funds, though most of their funds have a $3,000 minimum. Once your account is up and running, additional investments carry minimums of between $1 and $1,000.

Best of all, there are no commissions involving trades of Vanguard mutual funds. There are commissions for non-Vanguard funds and ETFs purchased through the platform, but Vanguard has enough of its own funds that non-Vanguard funds will be unnecessary. And most likely, if you open a Roth account with Vanguard it will be primarily for the purpose of investing in Vanguard funds.

Brokerage Accounts

Albert didn’t mention brokerage accounts as a potential option, but I’m adding them since they should be considered. Many brokerage companies have excellent packages for Roth IRAs and offer the advantage that you can have a much wider number of investment options.

For example, not only do they offer individual stocks, but they also typically offer mutual funds, ETFs, commodities, bonds, and various other investments that may become more interesting as you expand your investment activities.

E*TRADE is an online discount brokerage firm, that tops my list of brokerage accounts for a Roth IRA, because they have one of the lowest fee structures in the industry, in addition to being one of the highest-rated brokerage platforms on a consistent basis.

There is no minimum required to open an account and no set-up, maintenance, or close-out fees. They charge a commission of $9.99 per trade on stocks and ETFs, and $19.99 on mutual funds. Speaking of which, they offer more than 1,000 mutual funds that have both no load and no transaction fees.

TD Ameritrade is also an online discount brokerage firm that now includes the former broker Scottrade. With TD Ameritrade, you get access to investing tools and a robust offering of stocks, ETFs, and mutual funds.

Their commissions are low – $0 for stock and ETF trades, no commission for mutual fund trades, and $49.99 for no-load mutual funds. There is no account minimum deposit for a Roth IRA, nor is there a minimum balance requirement. TD Ameritrade also charges no fees for account set-up or maintenance.

Ally Invest is another online discount brokerage and stands out as having one of the lowest stock trade commissions available. This is an excellent platform if you are an active trader.

For example, Ally Invest offers commissions on stocks and ETFs of just $4.95 per trade and $9.95 per trade on mutual funds. There are no fees for account set-up, and there is no minimum balance requirement to open an account.

Betterment isn’t a brokerage account like the firms listed above, but a robo-advisor platform that manages your investments for you for a small fee. Betterment is the perfect choice if you are a hands-off investor who prefers to have professional investment management.

Betterment creates a portfolio for you based on your age, investment time horizon, and risk tolerance. The portfolio is created from a small number of ETFs that represent the entire global stock and bond markets. Once the portfolio is created, they automatically rebalance it for you as needed.

There are no transaction fees, but there is an annual fee based on the size of your investment account balance. For example, they charge 0.35% for an account balance of under $10,000, 0.25% for a balance of between $10,000 and $100,000, and 0.15% for account balances of $100,000 or more.

That means that you can have a fully managed account with a balance of $100,000 managed for just $150 per year. There is no minimum account balance required.

You can even open an account with no money, so long as you commit to funding the account with a minimum monthly deposit of $10. Overall, this is probably the lowest-cost way to have a professionally managed investment account.

But Don’t Forget Albert – There are Taxes on a Roth IRA Conversion

Since Albert’s question involves converting his 401(k) plan to a Roth IRA, I do feel that I need to emphasize the tax implications. Whenever you convert a tax-sheltered retirement plan – other than another Roth IRA – to a Roth IRA, there is the potential for having to pay income taxes on the conversion.

So Albert, if you’re going to convert your 401(k) into a Roth IRA, please be aware of this tax liability. I’d also recommend that you consult with a CPA if the amount of the conversion is particularly large, and will cause a big tax bill. There may be ways to minimize that.

Otherwise, any of the accounts listed above will be excellent places to set up a Roth IRA.

Bottom Line – Best Roth IRA Choice: Credit Union or Mutual Fund?

Choosing the right place to roll over your 401(k) to a Roth IRA is crucial. Credit unions and banks offer safety but may not provide significant growth due to low-interest rates. Mutual fund companies, like Vanguard, offer low fees and are optimized for mutual fund investments. Brokerage accounts, such as E*TRADE, TD Ameritrade, and Ally Invest, offer diverse investment options, while robo-advisors like Betterment provide hands-off, professional management.

However, it’s essential to remember that converting a 401(k) to a Roth IRA can have tax implications. Consulting with a CPA can ensure a smooth transition and help navigate potential tax liabilities.

I don’t understand my credit union Roth IRA at Navy federal is 3.75% but with TD Ameritrade, it’s 0 to 1% with fees. And the rollover for a Credit Union is free. I know Credit Unions are safe but aren’t you losing more money with a brokage account, with all the fees, penalties, and commisions.

Hi Vince – Is the 3.75% a CD? That’s pretty generous, even with rising rates. But the point is a credit union is where you’ll get fixed rate investments, and that part is fine. But a brokerage, like TDA, is where you can invest in stocks, mutual funds, etfs – growth assets. So yes, you’ll generally pay more for a brokerage in one way or another, but they do provide other advantages.